Double-digit health insurance premium hikes can quickly drain a company’s cash flow. Many Washington business owners endure mediocre benefits service because they fear plan disruption. However, replacing your advisor does not require changing your actual insurance plans.

Upgrade your benefits advisor before renewal: Schedule a complimentary WHIA review.

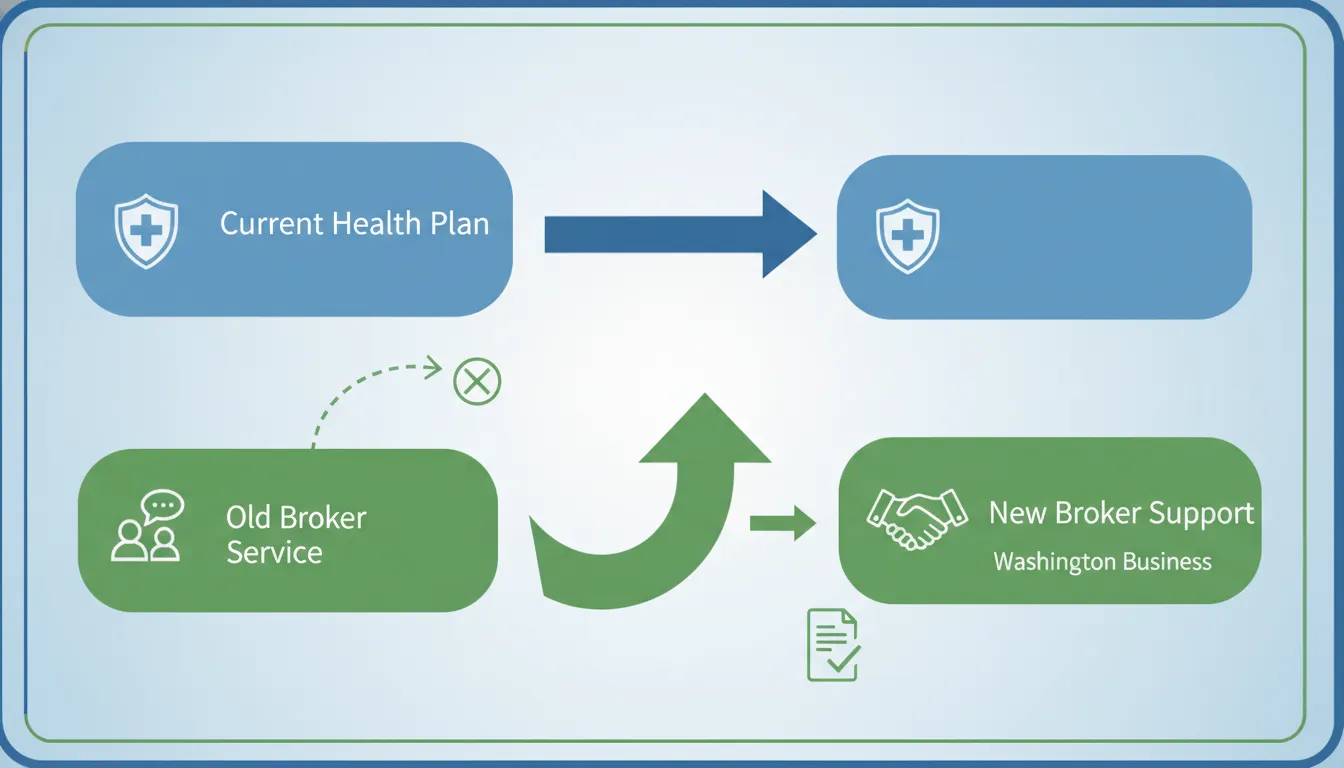

A broker of record letter Washington businesses sign is a legally binding document designating your new advisory partner as your exclusive representative with insurance carriers. This administrative tool allows employers to switch benefits advisors at any point during the year without changing their existing insurance plans or disrupting employee coverage. It formally terminates your relationship with your previous firm and transfers all policy management and carrier communication privileges to your new benefits partner. By executing this document, your business gains access to deep strategic support and tailored benefits optimization while keeping your current plans completely intact. The entire transition requires zero disruption to your employees, costs nothing to implement, and immediately upgrades your daily service model.

Many Washington employers wonder how this transition affects their daily benefits operations and ongoing carrier relations. To understand how this administrative shift impacts your company, start with what a broker of record letter changes and what it leaves untouched.

Broker of record letter Washington: what it changes

Many employers want to switch their benefits partner but fear that doing so will disrupt coverage. You do not have to worry about losing your insurance plans. A broker of record letter Washington is the industry-standard method for transferring control of an insurance policy from one broker to another. Using this simple document allows your business to change its advisory partner without any hassle.

Definition of a broker of record letter

A Broker of Record (BOR) letter is a legally binding document. It designates a specific broker as your exclusive authorized representative with insurance carriers. It does not alter your actual coverage or premium rates. Instead, the document replaces the previous broker’s service role and changes the agent of record for service and commission purposes.

This allows your new agent to approach insurance markets to obtain competitive quotes on your behalf. The new advisory partner assumes full responsibility for managing the insurance coverage for the business. They can begin to resolve administrative problems, handle renewals, and build a stronger plan.

Washington licensed producer rules

In Washington, health insurance plans must adhere to state laws. Proper administration of insurance documents is required for regulatory compliance under Washington state insurance laws. Under these rules, the Office of the Insurance Commissioner regulates employer-sponsored health plans to ensure consumer protection.

Your new advisory partner must be a Washington licensed producer in good standing. You can use state resources to verify their licensing status before signing any official document. Once appointed, your new broker accepts the professional liability for managing your policy. The former broker is usually entitled to the full annual commission regardless of when you file the letter.

The keep-your-plan upgrade option

Many businesses with 20-300 employees are underserved by large national firms, but they fear the disruption of changing benefits. The truth is that switching brokers does not touch your carrier contract. You keep your current medical plans, networks, and rates. The only difference is that you replace a silent, distant broker with a dedicated local expert at Washington Health Insurance Agency.

By filing a broker of record letter Washington, you can upgrade your benefits strategy without any administrative pain. Your new partner can focus on benefits optimization instead of just selling pre-packaged products. Your employees will not experience any gap in healthcare coverage. Also, your human resources team can get the daily support they need.

What changes for employees after the letter is signed?

Short answer: Employees usually see no change in their health plan, provider network, insurance cards, deductible, or copays. What changes is the service team behind the plan. The new broker takes over carrier communication, claims support, renewal strategy, and employee advocacy while coverage continues normally.

No disruption to existing healthcare plans

Many employers fear that changing partners will disrupt active benefit plans. In reality, signing a broker of record letter Washington keeps your existing coverage fully intact. With a structured broker transition, you will not face any disruption to coverage. Employees do not get new health insurance cards, nor do they need to find new doctors.

Your deductibles, out of pocket limits, and copays stay exactly the same. The insurance carrier relationships do not change because the carrier contract remains in place. Employer-sponsored health plans are regulated at the state level by the Office of the Insurance Commissioner in Washington. Working with a dedicated advisory partner like Washington Health Insurance Agency ensures a seamless shift.

Better service and dedicated advocacy

When you change servicing brokers, employees will experience no gaps in their active coverage. They can continue to see their current medical providers and pharmacies with complete confidence. While the insurance plan stays the same, the actual support employees receive improves. Our boutique agency rejects the volume-driven call center model of massive firms.

Instead, we offer personal care with direct access to senior expertise. Employees no longer have to struggle with long wait times to resolve basic benefits questions. Our team serves as a dedicated partner to resolve complex claims, billing errors, and coverage disputes. This direct line of contact takes the burden off your human resources team.

We solve real problems through benefits optimization rather than selling standard products. This transition allows your company to build a better strategy for future renewals. Our specialists study plan utilization to build a modern benefits package with cost-saving funding setups. We also bring complete transparency to agency compensation to cut down unnecessary broker fees.

Side-by-side comparison of the transition

Our team handles the administrative load so your staff can focus on daily operations. This model turns benefits from a chore into a reliable tool for retention. Knowing what changes and what stays the same helps ease any transition anxiety for your leadership team. While administrative details stay stable, the day-to-day service experience gets a major upgrade.

Here is a clear view of how a broker of record letter Washington impacts your group benefits. We compare how daily services and long-term planning look before and after the change. This side-by-side breakdown highlights the immediate advantages of upgrading your broker partner.

| Benefit Aspect | What Stays the Same | What Changes for the Better |

|---|---|---|

| Carrier & network | Your insurance carrier, doctor network, and plan designs do not change. | You receive a more proactive, local service model. |

| Employee cost sharing | Deductibles, copays, and out-of-pocket maximums remain intact. | We look for long-term strategies to keep premiums from rising. |

| Service & support | Your current policy terms and coverage limits stay in place. | Employees get direct access to senior expertise instead of call centers. |

| Claims help | The carrier processes and pays all medical claims as usual. | Our experts handle claims disputes and billing questions for employees. |

| HR administrative burden | Your HR team remains the internal contact for benefits. | We reduce HR work by managing plan setup and open enrollment details. |

How a broker of record letter Washington employers sign keeps plans intact

Short answer: The employer signs a letter on company letterhead appointing the new broker as the representative for existing carrier policies. The carrier processes the appointment, then grants the new broker access to manage service, quotes, renewals, and advocacy without replacing the active health plans.

Many mid-market businesses stick with mediocre brokers because they fear changing their insurance plans. This fear is common, but you do not need to replace your health plans to get better service. You can keep your existing employee benefits package while upgrading your administrative support. A seamless transition is possible when you follow the standard state procedures.

The function of a broker of record letter

The key to this transition is a document known as a broker of record letter. A broker of record letter is a legally binding document. It designates a specific broker as your exclusive representative with insurance carriers. This designation does not change your actual insurance contracts. Instead, a broker of record appointment only changes the agent of record for service and commission purposes. This simple shift allows you to maintain your current plans while gaining a more proactive service model.

Step-by-step transition process

A professional transition can be completed in a few structured steps. By taking control of this process, you protect your business and employees from administrative gaps. Here is the process for using a broker of record letter Washington employers should follow to switch partners.

- Review current broker service. You should assess how well your current partner handles issues. Look at their responsiveness during recent renewals or open enrollment. If you find a lack of strategic support, it is time to consider a change.

- Choose a licensed Washington advisory partner. Look for a boutique agency that offers personalized support. Before you sign any agreement, you should check their credentials. You can use resources from the Office of the Insurance Commissioner to verify their licensing status.

- Confirm specific carrier requirements. Some insurance companies have unique rules for processing broker changes. Your new advisory partner can help you review these rules. They will ensure that you meet any notice periods or formatting guidelines.

- Draft and sign the letter. Your new partner will help you draft the document. It must be printed on your company letterhead. The document must list the specific insurance carriers and plan numbers you want to move.

- Notify your insurance carriers. The new advisory partner will submit the letter to the carriers. Most carriers have a short waiting period to allow the previous broker to respond. Once this period ends, the carrier officially transfers the servicing rights.

- Transition open issues. Your new partner will take over outstanding billing questions or claims. They will review your current plan structure to prepare for your next renewal. This proactive review helps you find potential cost savings.

Carrier processing and compliance

Once the carriers receive your letter, they begin the official processing window. In Washington, employer plans are regulated at the state level by the Office of the Insurance Commissioner to ensure consumer protection. This regulatory oversight helps maintain a fair and transparent transition process. The carriers will usually complete the transfer within ten business days.

During this processing window, your daily operations will not change. Your employees can use their existing insurance cards without any coverage gaps. Your premium payments and claims submission processes will also remain exactly the same. The only difference is that your new advisory partner now has the authority to advocate on your behalf.

Frustrated with slow broker service? Schedule a WHIA benefits review before your next renewal.

What should CEOs and CFOs ask before signing?

Short answer: Before signing, leaders should confirm licensing, commission transparency, carrier access, service model, transition timeline, renewal strategy, and how the broker will protect employees from disruption. The letter is simple, but the advisory relationship behind it determines whether the switch creates real value.

Signing a broker of record letter Washington employers use is a quick task. But choosing the right partner requires real due diligence. A boutique firm like the Washington Health Insurance Agency can offer a tailored service model that larger agencies cannot match. Mid-market companies with 20 to 300 employees often face double-digit rate hikes each year. To avoid these costs, leaders must ask hard questions before they make a change.

A Broker of Record (BOR) letter is a legally binding document. It designates a specific broker as your exclusive authorized representative with insurance carriers. Employers use a BOR letter when they decide to switch their benefits partner and need to formally notify the insurance company of the change. This simple administrative step allows your new advisor to approach insurance markets to obtain competitive quotes on your behalf. It does not cancel your plans or disrupt employee coverage.

Broker qualifications and commission structures

First, you must check the regulatory status and licensing details of your new advisor. The state of Washington sets strict licensing and compliance rules for all insurance producers under state insurance laws. You should verify that your broker has an active license directly with the Office of the Insurance Commissioner. Next, ask about commission structures. Traditional brokers often hide their pay behind carrier bonuses. You want an advisory partner who provides full commission transparency. This clarity helps remove the sales bias that leads to higher premiums.

You can use these questions to audit a broker’s credentials and business model before you sign:

- Is your agency fully licensed in Washington, and do you have any complaints on file?

- Will you disclose all commissions, fees, and carrier overrides in writing?

- How do you handle the transition of service duties without interrupting our active coverage?

Service delivery and advanced funding plans

Many corporate leaders stick with mediocre benefits plans because they fear plan disruption. But a professional broker transition should be seamless for your HR team and your employees. You should ask how your new partner reduces this transition burden. A high-quality broker provides a direct line to senior experts rather than a routing system or call center. They should also focus on solving business problems through plan optimization instead of just selling insurance products. To see if you are ready to make a move, you can review these 10 Reasons to Switch Brokers.

Ask these strategic questions to evaluate their service model:

- Do we get direct access to senior experts, or will our account be sent to an account manager?

- What cost-saving advanced funding strategies do you use to control premium spikes?

- What is your exact timeline for our annual renewal process?

- Will you provide detailed strategy reports that show how our plans perform?

A well-planned broker change does not alter your actual coverage. It simply updates who services your policy and who receives the commissions. When you ask these questions, you ensure that your business gets the best possible service and strategy. A structured due diligence process helps you find a partner who will protect both your employees and your bottom line.

How WHIA manages a broker transition before renewal

Short answer: WHIA reviews your current plans, prepares the broker of record letter, coordinates carrier submission, handles open service issues, and begins renewal analysis early. The goal is to improve strategy and responsiveness before rates arrive while keeping employees on the same coverage.

Many business owners in Washington State hesitate to switch benefits partners. They worry that a transition will disrupt employee coverage or create extra human resources work. But you do not need to change your health plans or insurance carriers to get better support. A seamless transition is possible when you work with a dedicated team.

This process lets you upgrade your provider without altering your active benefits. Your employees keep their same network doctors and insurance cards. Your HR team also avoids the burden of setting up new insurance plans from scratch.

Minimizing transition disruption

For businesses with 20 to 300 employees, large national brokerage firms often provide basic, commodity services. These mid-market employers are often underserved by a volume-driven model. A boutique benefits advisory partner offers a personalized alternative. You can maintain your active plans while upgrading your level of service.

Our white-glove onboarding support manages transition details so your team does not have to do the work. This standard process focuses on three main priorities:

- Direct access to senior benefits advisors instead of dealing with junior call-center workers.

- Full transparency regarding commissions, costs, and strategic plans.

- Direct management of carrier communications to reduce the burden on your HR team.

This hands-on approach helps you avoid change fatigue. Your team keeps their coverage while you gain a strategic partner. You can read about the reasons to switch brokers to see how this transition improves your plan management.

Submitting the broker of record letter

To start this change, you must submit a formal document to your insurance carriers. A broker of record letter Washington employers sign officially transfers plan control between agencies. This document designates WHIA as your exclusive partner. It officially changes the agent of record for service and administrative purposes.

Signing this letter does not void your current insurance policies. It simply tells the carrier which agency will manage your plan moving forward. It also allows your new partner to contact insurance markets and gather competitive quotes for your upcoming renewal. Proper handling of these documents is important for compliance with Washington state insurance laws.

Preparing for benefits renewal

Once the transition is complete, renewal preparation begins immediately. We do not wait for carriers to send rate increases. Instead, our team looks at your current plan to solve business problems through benefits optimization. We analyze plan data to find places where you can control overhead.

We work to help you control costs. Our team reviews options like advanced funding strategies to improve your cash flow. We also look at plan designs that can help you avoid double-digit premium increases. This preparation ensures that your business is ready for open enrollment well before the deadline.

Common mistakes to avoid with a BOR letter

Bad timing and employee worry

Waiting until renewal pressure is high is a common pitfall. Many employers wait until they receive a double-digit rate hike before looking for a new partner. Switching during this busy period increases stress and leads to quick, poorly planned choices. You should start the process ninety days before renewals to give your new partner enough time.

Another error is assuming your staff must change insurance plans when you switch partners. A professional broker transition should be seamless for your team. When submitting a broker of record letter Washington employers should understand that the document does not void current contracts. You can keep your existing health plans while upgrading your advisory partner.

Licensing and commission blindspots

Signing a BOR letter without checking credentials is risky. You must confirm that your new partner is properly licensed to represent you. The Office of the Insurance Commissioner offers tools to check licenses on the insurance commissioner website. Failing to check licensing can lead to compliance issues under Washington law.

You must also check specific carrier rules before signing. Some insurance companies have strict requirements like a five-day notice period before a transfer is official. Under Washington state insurance laws, compliance with document standards is essential for regulatory adherence. You can read more about these standards on the Washington State Legislature website.

Many employers also ignore commission transparency. Some agencies operate with a commissions-based bias that impacts their advice. You should also know that the former broker is entitled to the full annual commission. You can learn more about this on the commission rules FAQ page.

Operational gaps and HR prep

Failing to transfer open service issues is a common oversight. If your staff has active billing or claim issues, they do not automatically move to the new advisor. A proper transition must include a detailed list of open tasks. The new agency needs to take over these issues to protect your staff.

Finally, many leaders do not set clear expectations with their human resources team. HR managers often struggle with administrative burden and broker unresponsiveness. Changing advisors without prep causes confusion during critical times like open enrollment. You must share your plans early so your team can work with the new advisor.

Starting the transition process early allows you to establish a strong roadmap. Your new partner should hold regular check-ins with your HR staff. This deliberate planning minimizes the administrative burden. It also guarantees that everyone understands their new roles before the contract begins.

Frequently Asked Questions

Does a Broker of Record letter cancel my current insurance policy?

No, signing this document does not cancel or void your active coverage. A broker of record appointment only changes the agent who manages your policy and receives the commission. According to the Washington Health Insurance Agency, your underlying insurance contracts remain fully intact. Your business keeps the same health plans, premium rates, and medical networks. The transition only updates your service team so you can secure better administrative support.

Does a Broker of Record letter affect the previous broker’s commission?

The previous agent usually retains their commission for the remainder of the policy year. In most cases, the insurance carrier pays the full annual commission to the firm that originally placed the coverage. As explained in the commission guidelines, filing this letter does not cut off their compensation immediately. The new advisory partner will manage your daily plan needs, but they typically do not collect commissions until your annual renewal date.

Can I use a Broker of Record letter to receive a quote from another insurance carrier?

Yes, signing this letter grants your new advisory partner the authority to represent your business in the insurance marketplace. This official designation allows them to negotiate directly with different carriers to find competitive health plans. Based on the market access rules, insurance companies require this formal documentation before they will release private group details. With this letter, your advisor can collect and compare customized rates for your business.

Does a new broker have professional liability exposure after a BOR appointment?

Yes, the incoming advisory partner takes on significant professional responsibility when they assume management of your benefits. By submitting the letter, the new advisor accepts full professional liability for administering the active plans. According to the liability standards, they become legally responsible for any compliance errors or plan management mistakes that occur under their watch. This exposure ensures that your new partner remains highly focused on maintaining accurate policy records.

Ready to upgrade your business benefits advisor today?

Remaining with an unresponsive advisory partner costs your Washington firm valuable time, administrative hours, and capital every single month. If you begin the administrative transition process today, your new advisory team can design optimized plan alternatives immediately. This proactive timeline protects your business cash flow and ensures your employees receive high-quality enrollment support before renewals.

Ready to protect your company benefits budget from rising premium costs and inadequate advisor support? Washington business owners do not have to settle for substandard service or frustrating administrative delays from traditional national agencies. Our experienced local team helps firms navigate complex state regulations and build sustainable, high-quality coverage plans. Schedule a complimentary benefits review with our experts today to secure better advisory services.