The annual contribution limitations for health savings accounts (HSAs) and high-deductible health plans (HDHPs) are increasing for 2019 according to Revenue Procedure 2078-30. HSAs are subject to annual aggregate (employer + employer) contribution limits. In order for an employee to contribute to an HSA, he or she must be enrolled in an HDHP meeting minimum deductible and maximum out-of-pocket thresholds. HSA participants age 55 or older are allowed to contribute additional catch-up contributions.

The contribution, deductible and out-of-pocket limitations for 2019 are shown in the table below (2018 limits are included for reference).

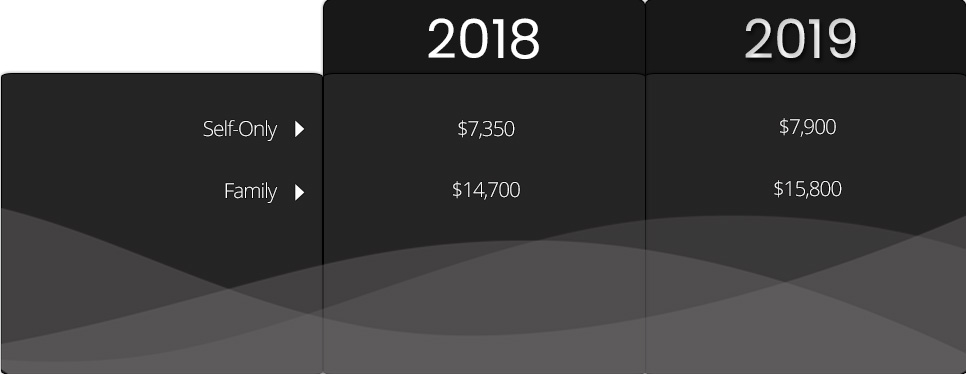

Note that the Affordable Care Act (ACA) also applies an out-of-pocket maximum on expenditures for essential health benefits. However, employers should keep in mind that the HDHP and ACA out-of-pocket maximums differ in a couple of respects. First, ACA out-of-pocket maximums are higher than the maximums for HDHPs. The ACA’s out-of-pocket maximum was identical to the HDHP maximum initially, but the Department of Health and Human Services (which sets the ACA limits) is required to use a different methodology than the IRS (which sets the HSA/HDHP limits) to determine annual inflation increases. That methodology has resulted in a higher out-of-pocket maximum under the ACA. The ACA out-of-pocket limitations for 2019 were announced in the 2019 Notice of Benefit and Payment Parameters and are shown in the table below (2018 limits are included for reference).

Second, the ACA requires that the family out-of-pocket maximum include “embedded” self-only maximums on essential health benefits. For example, if an employee is enrolled in family coverage and one member of the family reaches the self-only out-of-pocket maximum on essential health benefits ($7,900 in 2019), that family member cannot incur additional cost-sharing expenses on essential health benefits, even if the family has not collectively reached the family maximum ($15,800 in 2019).

The HDHP rules do not have a similar rule, and therefore, one family member could incur expenses above the HDHP self-only out-of-pocket maximum ($6,750 in 2019). As an example, suppose that one family member incurs expenses of $10,000, $7,900 of which relate to essential health benefits, and no other family member has incurred expenses. That family member has not reached the HDHP maximum ($15,800 in 2019), which applies to all benefits, but has met the self-only embedded ACA maximum ($7,900 in 2019), which applies only to essential health benefits. Therefore, the family member cannot incur additional out-of-pocket expenses related to essential health benefits, but can incur out-of-pocket expenses on non-essential health benefits up to the HDHP family maximum (factoring in expenses incurred by other family members).

Employers should consider these limitations when planning for the 2019 benefit plan year, however we understand that all of these acronyms (HDHP, HSA, ACA) and all of the rules and limitations attached to them can be mind boggling! We provide this information to keep you updated, but REST ASSURED! We are here to guide you and your employees through the maze! We are dedicated to help you provide the best group health benefits, meeting both the needs of your company and those of your employees.